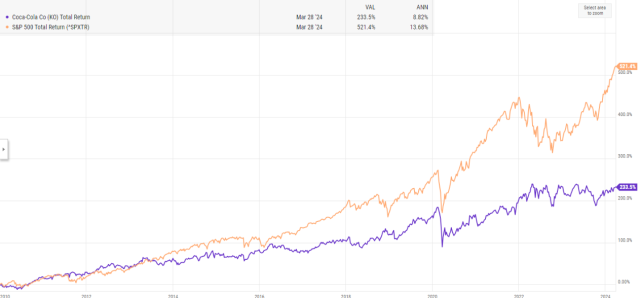

Coca-Cola Co’s (NYSE:KO) performance has been lackluster compared to the S&P 500 since 2010. However, as a consumer staple, it offers stability in revenue and earnings growth, albeit with modest returns.

Performance Comparison

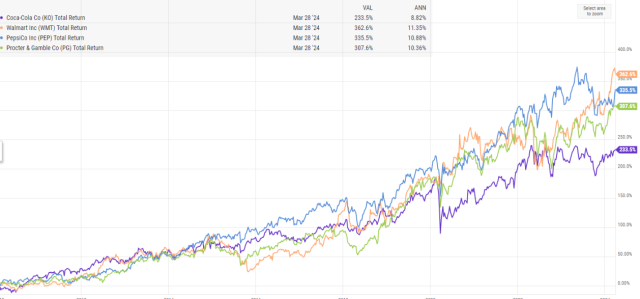

KO has underperformed Walmart (NYSE:WMT) and outpaced Pepsi (PEP) over the years. Despite its mediocre performance, it remains a staple in many portfolios due to its stability.

Earnings Expectations

Analysts expect $0.70 EPS on $11 billion revenue and $3.6 billion operating income, with marginal year-over-year growth.

Improving Operating Margins

KO aims to enhance operating margins, evident from its historical data. The spin-off of Coca-Cola Bottling was expected to reduce capital intensity and improve margins, signaling a strategic shift.

AI Integration

Coke’s recent strategic partnership focuses on aligning its technology worldwide, leveraging generative AI and cloud platforms. These improvements are anticipated to reflect in operating margins and free cash flow.

Valuation and Concerns

While KO trades at a premium with modest growth expectations, its 4% free-cash-flow (FCF) yield provides some appeal. However, concerns linger regarding the dividend’s absorption of FCF.

Despite efforts for innovation and strategic partnerships, Coke’s slow pace frustrates investors. While other consumer staples may offer better investment prospects, Coke’s future remains under scrutiny.

(Note: This analysis is for informational purposes only. Past performance does not guarantee future results. Investors should assess their risk tolerance and adjust accordingly.)