Options have become a popular asset type to make excellent profits; their value is based on the price of their underlying asset. A popular measure to judge options’ implied volatility is by calculating its Vega. Positive Vega options are usually future-dated; however, the Vega doesn’t always stay the same.

If you are a new trader, you might find the terms alien, but you don’t need to worry, as, in this blog, we will talk about Vega options and how you can trade them to generate excellent profits.

We have Ezekiel Chew with us to share his take on the subject; he is a world-renowned mentor who has helped thousands of students achieve excellent results in the investment world. Let’s use his knowledge for our benefit.

What is Vega Options

Vega is the measurement of an option’s price responsiveness due to the change in volatility of its base asset. The volatility includes the speed and magnitude of an asset’s price change. Vega measures the option’s price sensitivity when the implied volatility of the base-asset changes by 1%.

Vega options are divided into two types. Positive Vega options are usually for future dated options, mainly because investors pay higher importance to options maturing in the longer term due to their premiums. Any difference in the volatility of an underlying asset would create a bigger difference in the options price.

The second type is negative Vega options; they usually involve options retiring within a shorter span. These options typically carry lesser premiums and low implied volatility, leading to a negative Vega.

Basics of Vega

The information about Vega options would have simplified the measure for you, but let’s understand the fundamentals of Vega. Greeks first used Vega in options analysis; they used it to evaluate an option’s price sensitivity and how the option price would change if the price of the underlying asset alters.

The first aspect of Vega is the option’s price sensitivity; an option is a derived asset, so its value is based on the price of an underlying asset. The underlying asset could be a foreign currency, stock, bond, or other REIT. Usually, the change in the underlying price would explain the difference in the option price.

The second aspect of Vega is the implied volatility of the underlying price; volatility can be simplified as the speed and magnitude of fluctuations of an asset. An asset is considered highly volatile if the asset changes significantly in a short span. Established companies usually have lower volatility than blue chips.

Vega uses both aspects to measure the option’s price sensitivity caused by a 1% change in the underlying asset. Usually, long-term options have higher premiums between the bid-ask spread that lead to a higher interest from traders. Maturing options are relatively less profitable, and traders may see the spread shrinking.

Vega can also determine market competitiveness for certain options; an option is considered market competitive if its Vega is higher than its bid-ask spread. However, if the Vega is lower than the spread, the opposite is true. Let’s dive deeper into how Vega creates a difference.

Implied Volatility

The options pricing model is used to determine the probable value of an option termed as premium; it identifies whether an option would end in the money. The premium provides trader’s with a theoretical probability about an option’s profit potential, helping them make a decision.

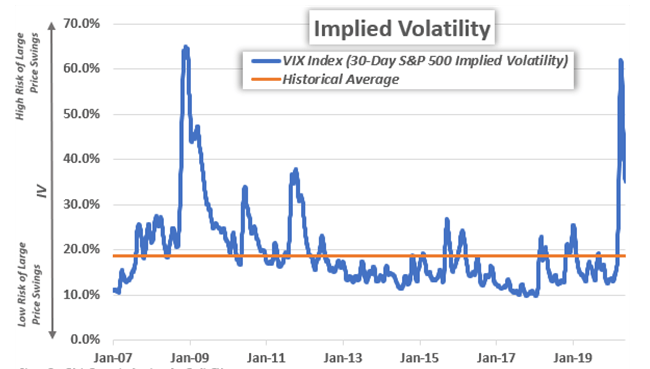

Implied volatility is a popularly used metric by traders’ to judge the probability of changes in an asset’s value. When calculating an underlying asset IV, we use the option pricing model. The goal is to account for the future volatility risk based on current market prices and ongoing conditions.

However, it must be noted that implied volatility isn’t a fixed value and may differ from original volatility. Similarly, the volatility value doesn’t stay the same when conditions change and may cause the Vega to alter.

As implied volatility increases, the vega value will decrease if price sensitivity stays constant. Summarily, the vega value is dependent upon the implied volatility of an asset; it gives us an indication of an option’s price sensitivity with different volatilities of the linked asset.

Vega Examples

We have talked about the two aspects of Vega; let’s now put our information to a fictitious example.

Consider a stock X trading at the market price of $20 in August; a call option of $24 in January has a bid of $ 1 and an ask of $1.05. Assume the Vega of the call option is 0.25 with an implied volatility of 25%. A Vega of 0.25 means that a change in implied volatility by 1% would cause the value of the option to alter by 0.25.

If the implied volatility of stock X increases to 30%, the option price will change by 1.25. In our case, the option’s bid should rise to 2.25, with the ask rising to $2.30. Our option is market competitive, as its Vega is bigger than the bid-ask spread.

However, market competitiveness doesn’t make it a viable option to invest in; you should have a detailed understanding of its prospect and how stock X’s value will possibly move.

How to Use Vega

A Vega can be used to determine the profitability of an option; a positive Vega usually exists for a long option. It is mainly due to the variation in implied volatility and the option’s premium. Experts use the option pricing model to determine an option’s premium, which will vary as the market factors for the underlying asset change.

A buyer would usually look for an option at a low premium and sell it when the premium rises; the opposite goes for a short seller; they would wish for the premium to decline to make a profit. When the implied volatility increases, the market premium increases, and if the implied volatility decreases, the premium follows the same pattern.

Hence, long options usually have higher implied volatility connected with them, leading to a higher premium and Vega. On the contrary, short options have lesser implied volatility, leading to a negative Vega.

Implied volatility of any option is based on the fluctuations in the primary market; a market with high fluctuations and uncertainty will lead to higher volatility that raises the Vega. While improved information and market stability reduce volatility, reducing Vega.

Ultimately, investors must consider whether a short vega portfolio will be better for their investment objectives. The short portfolio is relatively stable against implied vol tailing; the premium on the option doesn’t move significantly and stays close to its intrinsic value. A long vega portfolio is the opposite, and you can have higher expected volatility.

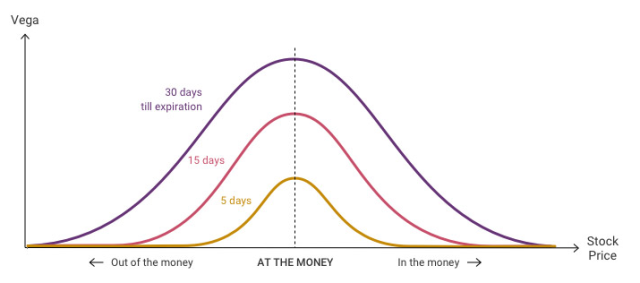

Options involve risk, and a successful portfolio requires a good balance between risk and return. Your portfolio should contain a mix of high and low vega options to stimulate risk and bring better returns. Options are highly risky when the underlying price is near the option’s strike price, also known as the money option.

Market swings can have various implications for traders, and you must organize your portfolio with diversified expiration dates so profitable deals can be materialized.

What is Vega used for in Options?

Vega plays an essential role in identifying the current price of the options and its potential to rise as the expiration date approaches. Traders use Vega to decide their positions for a trade. Markets are usually volatile, and traders can’t be sure about their movements.

Implied volatility plays a vital role in calculating Vega, ultimately deciding an option’s potential. Traders need to determine a market’s volatility to position their trades. If the market has higher implied volatility, it will lead to a higher profit by longing the option, and they would opt for it.

However, if the market volatility declines, they would choose the other way and short the option to gain better returns. Vega provides insights into an option’s profitability, and traders monitor its fluctuations to profit from perfect timings.

What are the Alternatives to Vega

Vega has multiple benefits in determining an asset’s profitability; it can help you abstain from an out-of-the-money option and invest in better-suited options. However, a few alternatives can still help us evaluate market fluctuation and make informed decisions.

The name of the indicators is based on Greek verbiage.

Delta

Delta measures the sensitivity of the price in relation to its underlying stock. It identifies the percentage change in options value after a 1% change in stock price.

Gamma

Gamma measures the rate of change of an asset’s data and the underlying asset’s price change. It uses delta to compare the time taken by the fluctuations in underlying assets to influence the stock price.

Theta

Theta is a measure of an option premium; it evaluates how the value of an option decays as it approaches its expiration date.

Rho

Interest rates offer a riskless investment pathway and play a role in an investor’s decision. Rho measures the change in option price due to a change in interest rate; it identifies the impact of a 1% change in interest rate.

Best Forex Trading Course

Traders have used Vega to decide their trading positions. A positive vega indicates high market volatility, making it favorable to take a longing trade and vice versa. The investment world has various other indicators that play a fundamental role in determining market changes.

Newbies must learn about the investment market before they set their foot in. However, they are often confused about the best course to seek guidance, as there is numerous investment advice on the internet, but they aren’t always beneficial. Asia Forex Mentor is our choice.

The course takes you through a comprehensive five-step procedure that details market movements, analytics, indicators, and conditions; the course summarizes the learnings of the year into a brief discussion that can answer your queries about a profitable investment.

The course mentions indicators and information backed by mathematical probability, making it highly reliable and trustworthy. However, the course’s credibility can only be affirmed by its creator- Ezekiel chew, who is regarded as the #1 Forex Mentor.

He has developed a unique course that teaches learners about market dynamics excitingly. He has trained thousands of students, and his technique helps them make six figures per trade relativity. DBP- the second largest bank in the Philippines- was also trained by Ezekiel Chew.

4 Best Forex Broker

Conclusion: Vega Options

Options trading provides traders an excellent opportunity to make a decent profit with considerably lesser investments. However, it requires mastery of market trends and indicators to avoid losses. Vega is a fundamental tool for options investors as it helps them evaluate the potential of an option.

Vega compares an option’s price sensitivity against the implied volatility of the underlying stock. If higher implied volatility occurs, the options premium will rise, leading to a higher Vega. The opposite is also true.

Traders must have a firm grip on Vega and its alternatives to analyze market fluctuations and their impact on the derived options. An investment strategy should involve a well-diversified portfolio of high and low-Vega options to drive results with minimal risks.

Vega Options FAQs

What does Vega mean in Options?

Vega measures the price sensitivity of an asset after a 1% change in implied volatility of the underlying asset.

Traders use it to decide their trading positions; a positive vega suggests a future-dated option with higher implied volatility. It presents a chance for greater premiums, so traders take long positions.

Is high Vega good for Options?

High Vega is good for longing positions; it suggests high implied volatility that leads to higher premiums. High Vega options usually have a long-dated expiration, making them a high potential asset to purchase.

A low Vega provides an opportunity to shorten. With declining implied volatility, the option premium will also decrease, suggesting the possibility of shorting profits.

How do you use Vega in Options?

Traders use Vega to predict the option’s value; if a call option is trading below its strike price, it would have only an extrinsic value. Traders should only buy it if the expiration date provides room for improvement.

Vega helps traders examine future movements in an asset, and they can evaluate the implied volatility to predict changes in option value.